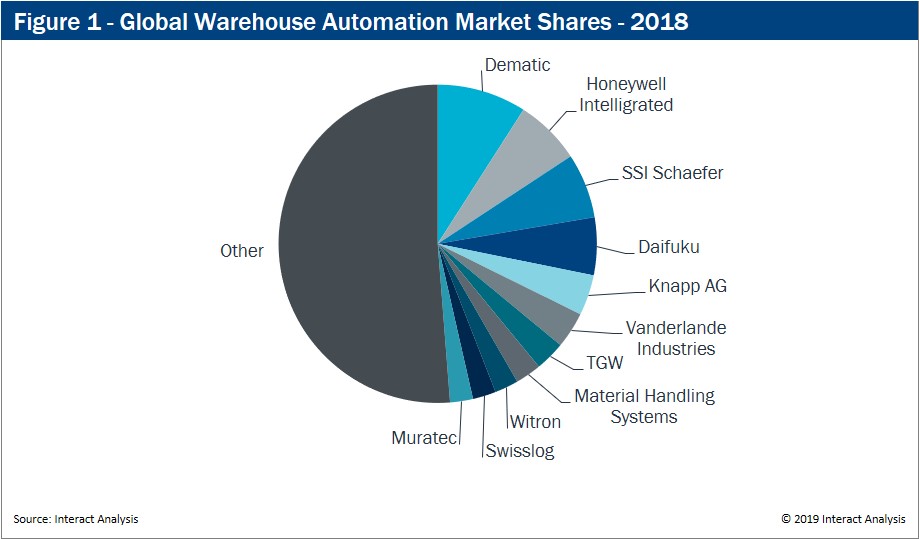

Dematic, which was acquired by KION in 2016, was the largest warehouse automation provider in 2018, according to Interact Analysis’ new report on this market.

The report found that Dematic held a 9% share of the global warehouse automation market, followed by Intelligrated (acquired by Honeywell in 2016), which held a 7% share (see Figure 1 above). The warehouse automation market exhibits the paradox of a highly consolidated landscape for larger customers and projects, yet at the same time extremely fragmented for smaller projects.

Dematic and Honeywell Intelligrated have been particularly successful within the general merchandise sector in recent years, with both companies winning large projects with e-commerce retailers. In 2018, Dematic and Intelligrated ranked No. 1 and No. 2 globally for general merchandise warehouse automation, respectively, in terms of revenue. In 2018, Dematic’s order intake grew 15.5%, while we estimated that Intelligrated’s revenues rose by more than 50% during the same period.

KION and Honeywell’s acquisitions form part of a wider trend of large industrial players entering the high-growth warehouse automation market, as well as consolidation occurring within the supplier base.

In addition to the moves made by Honeywell and KION, Toyota Industries acquired Bastian Solutions and Vanderlande in 2017, and it now holds the fifth largest share of the global warehouse automation market when combined. Similarly, Swisslog, ranked 10th globally, was acquired by robotics company KUKA in 2014.

With the global warehouse automation market forecast to experience a compound annual growth rate (CAGR) of 12.6% through 2023, with strong underlying drivers of demand, it’s easy to see why industrial companies have been striving to gain a foothold in the market. Warehouse automation in many ways complements their businesses.

For example, Intelligrated now offers Honeywell’s Connected Assets predictive analytics platform within its conveyor systems. KION and Toyota Industries have been able to use their European and U.S. sales and service networks and at the same time can sell complementary products such as fork trucks.

It’s not just industrial companies which are trying to get a piece of the action. In recent years, private equity firm Thomas H. Lee Partners has been on an acquisition spree acquiring Material Handling Systems, along with VanRiet, OCM, and a myriad of smaller engineering firms. This created the largest warehouse automation system integrator for the parcel sector ahead of second- and third-ranked Fives Group and Vanderlande. Its latest acquisition of AutoStore in June only strengthens its warehouse automation arsenal.

SSI Schaefer leads Europe, but competition is growing

While Dematic leads the global warehouse market, an estimated two-thirds of its business is in the Americas. SSI Schaefer on the other hand, is the European market leader with revenues in the region nearly 50% greater than its closest competitor, Knapp. However, a handful of European system integrators are closing in on the gap.

Knapp, which generated revenues of approximately $650 million in 2017, broke the $1 billion mark in 2018, a 63% increase. TGW has also seen phenomenal growth in recent years growing from approximately $550 million in 2015 to just under $800 million in 2018, although some of its revenues come from equipment sales to other system integrators.

In addition, Interact Analysis expects Honeywell Intelligrated’s European presence to increase during the next few years, following its acquisition of Transnorm in October 2018. Honeywell Intelligrated had a strong presence in both LogiMAT and IMHX, two of the largest European intralogistics trade shows, which may be a sign of things to come.

![]()

The Robot Report is launching the Healthcare Robotics Engineering Forum, which will be on Dec. 9-10 in Santa Clara, Calif. The conference and expo will focus on improving the design, development, and manufacture of next-generation healthcare robots. Learn more about the Healthcare Robotics Engineering Forum, and registration is now open.

APAC: The Wild East of warehouse automation

Whilst Europe, the Middle East, and Africa (EMEA) and the Americas have a relatively consolidated warehouse automation supply base with the top four system integrators accounting for 41% and 52% of the regional markets respectively, the Asia-Pacific region (APAC) tells a different story.

Although more than double the size of its closest Asian competitor, Daifuku is the market leader in APAC, yet it accounts for just 10% of the market. In fact, the top four system integrators in APAC account for just 19% of the regional market. This is primarily due to a very long tail of system integrators in China, many of which have only installed two to three projects. China’s warehouse automation market is made up of three distinct parties:

- Enterprise Integrators: Amazon rivals Alibaba and JD.com are two of the largest purchasers of warehouse automation in China. Instead of using system integrators to install automated warehouses, these companies, along with several other Chinese e-commerce retailers, tend to purchase automation equipment directly from equipment vendors and install the system themselves.

- Foreign system integrators: SSI Schaefer, Dematic, and Swisslog, along with several other foreign system integrators, are present in China and are often used for large scale automation projects in retail verticals.

- Local System Integrators: Lastly, local system integrators form the long tail with only a few companies such as Sinsun, Noblelift and Kunming Shipbuilding Equipment having revenues greater than $100 million.

Warehouse automation to grow despite challenges

Despite a slowing global economy, the warehouse automation market remains fairly resilient to the macro conditions due to the underlying structural drivers; the phenomenal rise in e-commerce – especially within APAC, the consumer demand for ever shorter delivery times and the on-going labor shortages.

Many warehouse automation vendors saw a strong rebound in order intake in Q3, reversing the first half of the year’s poor performance. As industrial companies prepare for a global economic slowdown, warehouse automation will be a key business unit for revenue growth.

About the author:

About the author:

Rueben Scriven has a first-class degree in biochemistry from Durham University. He is using his background in science and computer modeling as a member of Interact Analysis’ growing team.

This article republished with permission from Interact Analysis. For more information on the firm’s warehouse automation research, visit its report page, or contact it.

Tell Us What You Think!