AutoGuide Mobile Robots MAX N10 Tugger. AutoGuide was recently acquired by Teradyne. | Credit: AutoGuide Mobile Robots

Teradyne built its business around automatic test equipment for electronics. This still accounts for 75% of the $2.1 billion revenue Teradyne made in 2018. This is a mature market that is unlikely to yield significant growth in the long-term future.

As a result, Teradyne embarked on a series of acquisitions for key industrial robotics start-ups. With the acquisition of autonomous mobile robot (AMR) developer AutoGuide, Teradyne now has four major robotic vendors under its wing:

Universal Robots: Bought for $285 million in 2015, Universal Robots (UR) is the largest part of Teradyne’s Industrial Automation business. UR is the dominant cobot manufacturer, and through a combination of a massive distributor network and an effective integration platform (UR+), it grew to $234 million in revenue by 2018, with over 34,000 cobots sold as of mid-2019.

Mobile Industrial Robots: Acquired in 2018 for $272 million, Mobile Industrial Robots (MiR) develops AMRs for material handling in the intralogistics space.

Energid: Energid is focused heavily on motion control software. They were purchased in 2018 for an undisclosed fee and is likely Teradyne’s smallest robotics acquisition.

AutoGuide Mobile Robots: Bought for $58 million, AutoGuide develops autonomous tugs, forklifts and pallet stackers.

The AutoGuide acquisition was considerably cheaper than MiR as AutoGuide is at a much more nascent stage of development. When MiR was acquired, it had revenues of $12 million in 2017. AutoGuide hit $4 million in revenue for 2018. The fleet size is also considerably smaller. MiR has thousands of AMRs deployed across the globe, while AutoGuide hopes to ship 80-100 robots in 2019 and is planning to scale up to 200 for 2020.

But despite being at an earlier stage of development, AutoGuide offers something MiR does not: automation of heavy-payload specialized vehicles like pallet stackers, tugs and forklifts.

And AutoGuide can achieve this through one modular vehicle base that can be customized to perform different tasks. AutoGuide says it takes as little as four hours to change a pallet stacker to a forklift. Modularity is built into the entire AutoGuide technology stack, with seamless integration into various management and execution systems as well as programmable logic controllers (PLCs). There are plenty of options for customized reporting packages and access to specialized applications via APIs. AutoGuide does not rely on ROS for its architecture and has a bespoke vehicle traffic solution based on 2D navigation.

Much like UR and MiR, AutoGuide will be monetized primarily through reselling via distributors. AutoGuide also has a strategic partnership with system integrator Heartland Automation, though it is focused solely on the American market at the time.

Credit: Rian Whitton, ABI Research

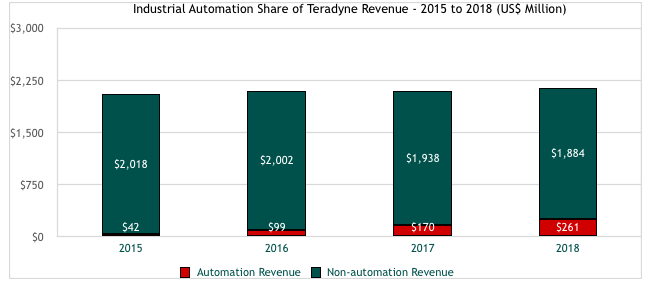

Teradyne’s Industrial Automation business

Automation is still a peripheral part of Teradyne’s business as far as gross revenue goes. But it is becoming more important with every investor meeting. In 2015, industrial automation represented 2% of all revenue, but industrial automation represented 12% of revenue in 2018. Teradyne hopes its automation unit will be posting revenues exceeding $1 billion in 2021.

Credit: Rian Whitton, ABI Research

Such predictions would likely have been qualified following 2018. While this was a successful year of growth at 54%, the $261 million haul was $20 million short of what was expected. This was due to a decrease in UR’s growth from 72% in 2017 to 38% in 2018, primarily a result of declining optimism in the automotive supply chain and general uncertainty about manufacturing growth worldwide. However, MiR performed well and maintained strong growth throughout, growing from $6.5 million in quarterly revenue to $10 million.

Overall, MiR has outperformed UR since being acquired. This is unsurprising given its smaller fleet size, but the fact that MiR has weathered economic uncertainty better suggests autonomous mobility is a safer bet for avoiding stunted growth than collaborative robots.

Credit: Rian Whitton, ABI Research

In 2018, MiR represented 9.2% of industrial automation revenue for Teradyne. For the first three quarters of 2019, it represents 14.3% of industrial revenue. With the acquisition of AutoGuide, Teradyne’s reliance on the cobot market will be diluted. Teradyne will transition to a more comprehensive robotic technology provider.

Of course, industrial automation remains only a part of Teradyne’s business. The main market remains semiconductor testing, with system and wireless testing being peripheral businesses. Automation revenue has grown from 2% in 2015 to 12% in 2018 and will be over 13% in 2019.

This trajectory likely means Teradyne will not reach its goal of a $1 billion automation business by 2021. But with AutoGuide’s acquisition, Teradyne has all the competencies needed to strengthen its position in intralogistics for manufacturing, where it is the dominant AMR actor. Importantly, Teradyne has been an early mover in both AMRs for material handling and for cobots. It is moving faster than most players in these respective markets.

But challenges abound. While Teradyne is gaining more traction in Asia, it is still reliant on the performances of the US and EMEA markets. Not withstanding this, Teradyne has effectively achieved a significant pivot from a mature industry (testing) with little prospect for growth, to becoming a major automation player.

About the Author

Rian Whitton is a research analyst for ABI Research, a market intelligence company focused on the most transformative technologies and their impact across industrial, commercial and consumer markets. As part of the Strategic Technologies research team, Rian provides an analysis for Robotics, Automation, Intelligent Systems, Artificial Intelligence and Machine Learning. He has also written actively on the commercial application of unmanned aerial vehicles. He has been a speaker at the Robotics Summit & Expo, produced by The Robot Report, and regularly contributes to media outlets like Bloomberg, Thompson Reuters, ZDnet, Recode and the Financial Times.

Prior to ABI Research, Rian graduated in 2017 with a Master’s degree in Science & Security from King’s College London, researching the intersection of technology and defense. He has chaired panels on and spoken at academic events about the intersection of technological innovation and defense, particularly in relation to AI and Robotics.

Tell Us What You Think!