Amazon’s purchase of Zoox was the largest robotics startup deal of 2020 so far.

With the frenetic first half of 2020 over, what’s the outlook for robotics startups that are fundraising in the midst of the pandemic? Great question. Most venture capital firms spent the end of Q1 and the first part of Q2 triaging their existing portfolios, understanding runway and cash needs, and working with management teams to reduce costs and pivot strategies where relevant. I’ve recently been on the fundraising trail with a couple of my portfolio/advisee companies and spoken to a number of early, mid- and late-stage investors that have invested in robotics startups. Here are some of the things I’ve learned:

Deals are still getting done

Robotics deals are still being made, but it’s taking longer and on terms that are less favorable than pre-pandemic. As one VC put it, before the COVID-19 pandemic, the pendulum had swung way toward the entrepreneur; it has now swung back the other way. In his opinion, deals are at a fairer equilibrium. Reasons cited for the longer deal cycles include the following:

- Investors need to reserve more dollars to support existing portfolio companies, especially their winners. So new robotics startups are competing with existing investments for the same pool of dollars.

- VCs lack the bandwidth to make more deals. As one founder put it, “I’ve heard several totally up my alley, and I definitely see it, but I already have two diligence processes going right now and am maxed out.”

- Longer due diligence. Processes that used to take two weeks now take six weeks.

- Partners are often unable to build the conviction to do a deal, having only met the founders remotely. “Several waste a lot of time by investing heavily in diligence and then deciding that it’s just too hard to build enough conviction remotely,” said one venture capitalist. At the same time, it’s understandable that physically seeing a robotics deployment in production is a lot more credible than a video demo. Software-only startups have it easier in this regard.

- VCs are waiting to see if valuations take more of a hit as time goes by. Some firms think it will only be a matter of time before distressed assets are out there and are taking a wait-and-see position.

- Some VCs are themselves fundraising and are distracted by this, or their LPs themselves have faced a capital crunch. I’ve seen at least a couple of fundraisings get drawn out due to the VCs’ inability to close on time due to their LPs’ inability to fund.

Still, deals are getting done. It may be that there’s a selection bias, where only the fittest robotics startups are braving the fundraising trail, while others regroup, pivot, and make their runway longer to fundraise when they have a better story.

Source: PwC CB Insights Money Tree Report Q2 2020

Flight to quality and looking for the ‘next big thing’

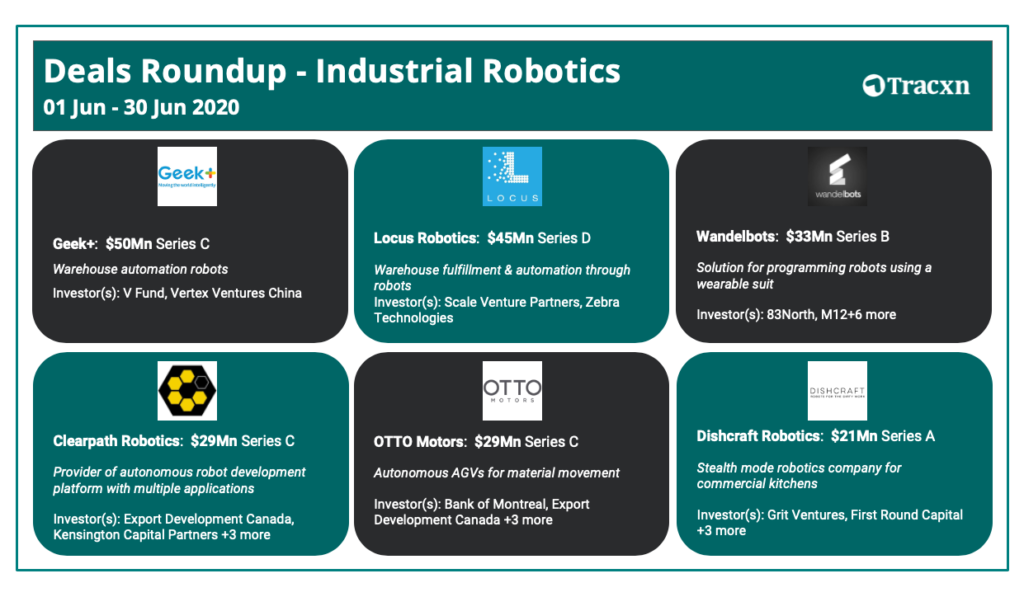

Typical of downturns, investors are doubling down on the winners — those with proven value propositions and a repeatable business model — and are putting more money to work in fewer startups. Witness the recent rounds of Geek+, Locus Robotics, and OTTO Motors. A well-known banker reported that, year on year, the first half of 2020 had 10% fewer deals but was up 25% in terms of dollars raised.

Some robotics categories are passé and no longer the next big thing. “It’s not 2016 anymore,” said one VC. What he meant was that there are emerging winners in categories like autonomous mobile robots and bin picking, so they’re looking elsewhere for “what’s next.” Others are putting money into robotics startups that will benefit from pandemic behavior changes like food assembly.

There’s a barbell effect that may lead to a Series A crunch. Traditional Series A investors may go upstream and make smaller bets to have more dry powder. Others may go downstream and bet on emerging winners to take lower risk. Both means there may be good companies that struggle to raise Series A or B.

There is dry powder for robotics startups that can be breakouts. One late-stage player sitting on hundreds of millions in dry powder bemoaned the fact that even high-profile robotics companies are still stuck between $10 million and $20 million in revenue. Even 6 River Systems was in that range when it got bought by Shopify. They’d love to see these break out and then get behind them in a big way.

(Click here for a larger version.) Source: Tracxn

Lessons for robotics startups seeking capital

First, this puts paid to the expression “Always be raising.” Robotics startups that have cultivated VC relationships pre-pandemic can lean on those instead of having to start new relationships remotely.

Get past pilots. Focus on hardening your platform versus delivering new features. For robotics startups in particular, Series A and beyond investors want to see a proven value proposition in production. They’ve seen plenty of companies with promising pilots that end up in purgatory. You need to convince them, ideally via reference customers, that you can get past pilots and into production. Unit economics matter when it comes to proving out the scalability of your business model.

Don’t forget existing investors. As obvious as it sounds, this may be the best time to do an internal round, even if it’s a bridge or at the last round’s valuation. Any potential negative signaling effects are mitigated due to the pandemic, and your investors are already gearing up to support you (see above).

Find alternative funding sources. From PPP loans and lines of credit from a bank to grants or customer pre-payments/financing, there are alternate routes to having enough capital to get to the proof points needed to do the next raise.

The good news is that robotics and automation are genuinely going to accelerate in the coming years, as the cultural barriers to adoption fall away during the pandemic. You just need to have the runway to ride that wave. Good luck, and godspeed.

About the author

About the author

Rags Gupta is a serial entrepreneur and operator. He was most recently the chief operations officer at microlocation provider Humatics Corp.

Tell Us What You Think!