A robot tax is a solution to a problem that doesn’t exist, namely the threat of mass joblessness through technology.

After South Korea’s reduction of tax-incentives for investment in advanced automation technologies, there is increased political support in both the UK and US to implement taxation on robotics. But pursuing a robot tax is an onerous path, built on faulty assumptions about job losses and a misdiagnosis of the problems ailing US and UK economies. The problem is not too much churn due to technological innovation, it is not enough.

Robot tax: what is the Problem?

First it is important to consider the justification for a robot tax; the threat of robotics and other technologies (broadly termed under automation) destroying jobs. This is a popular message among the punditariat, to the point where publications like The New York Times misrepresent academic studies to propagate the notion that manufacturing employment was not destroyed by the China shock, but by too much technological innovation.

An increasing assortment of evidence flatly contradicts that claim. Economists Restrepo and Acemoglu’s work indicated that robotics led to a mild decrease in US employment (670,000 jobs in between 1990 and 2007; 40,000 jobs each year, or a 0.34 percentage decline in the share of a working age population with a job). Other reports, like those of ABI Research, find the number of job losses in the US to be smaller, and even envision net growth from the expansion of the robotic ecosystem and increased productivity. Further work from ITIF finds that the churn of jobs lost and gained by technological disruption is at a record low in the US.

However, this was dwarfed by the offshoring of jobs to China, while automation as a whole actually led to job growth. Acemoglu and Restrepo confirm this in their study, with China’s WTO ascension having at least three times the negative impact on US jobs as robotics. Another landmark study by economists including Acemoglu found competition with Chinese imports had cost the US 2.4 million manufacturing jobs between 1999 and 2011. Were it the case that these losses were instead the result of automation, why did a 33% loss in manufacturing jobs coincide with a 22% loss of manufacturing plants (78,000) from 2000 to 2014? Presumably these job-killing machines have to be working somewhere.

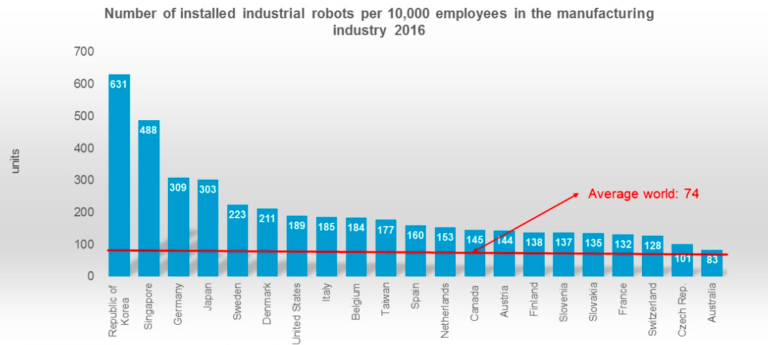

Companies that adopt robotics to a higher degree often retain a larger percentage of their manufacturing base than those that do not; for example, between 1993 – 2017 Germany, with a higher robotic density (number of robots per 10,000 manufacturing workers) of 308, lost 19% of manufacturing employment while the US, with a density rate of 196, lost 33% over the same period. The UK in particular was a laggard in industrial robot adoption, with a density rate of 70, and lost over 50% of its manufacturing employment in the same time period. As Harvard contributors Marc Muro and Scott Andes demonstrate, there is no significant correlation between robot deployment and job losses. Why tax something that has not been shown to be a job killer?

Related: 10 Most Automated Countries in the World

The problem here, outlined by Robert D Atkinson, is that when assessing the impact of robotics on jobs, people think about first-order effects but not second-order effects. They consider the loss of a worker due to the deployment of a robot for pick-and-place and machine-tending, but do not consider how the capital investment increases and productivity gains of robot deployment makes companies more competitive, increases market share and drives expansion – all of which require workers. The periods of highest productivity growth have been the healthiest for jobs. Capital investment growth correlates with new machine orders, which in turn correlates with productivity growth, which in turn correlates with new hiring and improved pay (due to increased market share). High productivity is a driver of job growth in an economy, not a subtractor, as efficient industries are magnets for investment and expansion.

It is also worth asking what would a tax on robots include? Many view robotics as a physical manifestation of AI. Are autonomous cars taxable? CNC machines? advanced machine tools? drones? If we realise that robotics are just one technology and automation involves thousands of sub-categories of technology, are there any limits to the tools and products that could be taxed for potentially negatively affecting job prospects? Should a retroactive tax be implemented to compensate the slaughterhouse workers who lost their jobs to the bandsaw? Should the descendants of peasants be compensated for the deployment of combine harvesters? I am being playful, but there is very little detail about the boundaries of what counts as a taxable machine, and the boundary is always contestable.

More Innovation, Not Less

The American economy has had significant structural problems over the last twenty years, in large part to bad policy that was often supported by both major parties. But being too receptive to innovative productivity-growing technology is not one of those problems.

For one thing, manufacturing output has stagnated, especially compared to countries adopting robotics a faster rate. Despite bipartisan belief that US industry has been roaring for the last twenty years, its output is roughly flat since 2000. There has not been a comparable period of stagnation in American manufacturing to the modern era. Where there has been extensive growth has been in computers and electronics. This supposed bright spot has been heavily overstated through the use of arcane statistical jiggery-pokery.

Susan Houseman of the Upjohn Institute found that the measuring of output does not merely account for the number of semiconductors or computers produced, but increases alongside their quality, so while the number of products produced could stay the same, or even decline, the output theoretically goes up. This, in effect, has provided the illusion of growth in manufacturing, when in fact, productivity growth, employment and share of global exports (including high-tech) are all down significantly.

Within this landscape, companies (including original equipment manufacturers and end-users) are already encumbered by significant costs relating to taxes and regulation. The 2017 Tax reform bill alleviated some of this burden by reducing America corporate tax rate from 35% to 21%, but new costs related to equipment spending (the robot tax) would stifle capital investment further, following years of limp investment growth. While global VC funding for fields like robotics and AI has gone up considerably, from $2.5 billion in 2014 to 12 billion in 2017, American general hardware capital investment growth in the US has slowed from an expansion of 16% between 1995 and 2002 to 8% between 2002-07 and 5% between 2007-16. A new tax on robotics would exacerbate this negative trend.

A look at the countries with the most automation in manufacturing industries. (Credit: International Federation of Robotics)

US capital investment growth in hardware is no isolated example of a slowdown. The story is remarkably similar for software investment and non-federal R&D spending. While business R&D investment in the United States jumped by two-thirds on an inflation-adjusted basis from $328 billion in 2000 to $458 billion in 2016, the rate of R&D growth as a share of GDP over the same period has been flat – inching up from 2.61 percent to 2.74 percent. If your economy is dependant on innovation as opposed to the low hanging fruit of a growing labor force, this is unacceptable. Moreover, businesses are investing a much smaller share of their revenues in riskier early stage basic and applied research than in later-stage development, and the global share of business R&D performed in the United States has fallen significantly in the last decade.

Anaemic growth in private sector R&D is troubling as it was supposed to compensate for stagnation in government R&D spending. In the 1960’s, US government R&D funding exceeded the rest of the world (public and private) combined. But since peaking in the late eighties at 1.2% of GDP, US Government R&D has fallen to 0.8% of GDP. Just as is true with robotic adoption, relative US stagnation is run counter to massive expansion among competitor economies. While US federal R&D increased by 3% from 2000-2012, China’s increased by 110%. Without significant change, relative decline of America’s historic advantage in technological innovation will continue.

The flattening of capital investment and R&D spending has come at a time when profits have been soaring. If anything, a punitive tax should be on those companies that do not increase technology investment, as opposed to those that do. At the very least, there should be increased tax deductions for R&D, especially for early-stage basic research, and the US should adopt an ‘innovation box’ tax policy that provides favourable treatment for revenues generated from new developed IP.

Must-Read: Why Bill Gates Thinks a Robot Tax is a Good idea

Conclusion

Good intentions are a low standard from which to judge a proposed policy. A robot tax is a solution to a problem that doesn’t exist, namely the threat of mass joblessness through technology. Despite the pessimistic consensus, evidence is mounting, via other countries and through a revised analysis of US automation efforts, that robotics will not cause a crisis in employment.

On the contrary, the US needs to accelerate its adoption of robotics to meet the challenge being posed by developed competitors like Japan, Germany and China. The role of government should be to incentivise increased capital expenditure on robotics, increase investment and productivity, and to develop a more expansive industrial policy to compete with other economies, not to impede technological adoption.

Within the US and greater Western world, we are an increasingly tepid and risk-averse society, bombarded with television, movies, novels and think pieces that saturate our culture with apocalyptic visions about how technology will destroy us, or at the very least liquidate our livelihoods. This obscures the fact that most of our problems don’t come from disruption, but from stagnation.

About the Author

Rian Whitton is a research analyst for ABI Research, a market intelligence company focused on the most transformative technologies and their impact across industrial, commercial and consumer markets. As part of the Strategic Technologies research team, Rian provides an analysis for Robotics, Automation, Intelligent Systems, Artificial Intelligence and Machine Learning. He has also written actively on the commercial application of unmanned aerial vehicles. He has been a speaker at the Robotics Summit & Expo, produced by The Robot Report, and regularly contributes to media outlets like Bloomberg, Thompson Reuters, ZDnet, Recode and the Financial Times.

Prior to ABI Research, Rian graduated in 2017 with a Master’s degree in Science & Security from King’s College London, researching the intersection of technology and defense. He has chaired panels on and spoken at academic events about the intersection of technological innovation and defense, particularly in relation to AI and Robotics.

Tell Us What You Think!