Business, technological, and social drivers, as well as the COVID-19 pandemic, have accelerated deployments of mobile robots in the warehousing and other sectors.

|

Listen to this article

|

![]() At the end of 2020, mobile robots were deployed in just over 9,000 separate customer sites. By 2025, deployments will increase to over 53,000 sites.

At the end of 2020, mobile robots were deployed in just over 9,000 separate customer sites. By 2025, deployments will increase to over 53,000 sites.

While this may seem like a great deal, it is not even close to reaching the ceiling of market saturation. Market penetration of mobile robots in 2025 will still not have exceeded 30% (Figure 1).

Furthermore, those penetration levels do not account for facilities where multiple types of robots installed, nor the mass rollout of fleets in a single warehouse. Given that, the market opportunity for automated guided vehicles (AGVs) and autonomous mobile robots (AMRs) is even greater.

Figure 1: Penetration of Mobile Robots (Deployments / Total Customer Sites) Source: Interact Analysis

The warehousing sector in particular is poised to become a huge market for mobile robot vendors. Research by Interact Analysis shows that 2020 marked a watershed for the industry. Growth resumed midway through the year, after a difficult first half amidst the height of the pandemic.

Despite capital expenditure (CapEx) restrictions and facility shutdowns, overall mobile robot shipments increased by more than 25% in 2020, and with nearly 60,000 AGVs and AMRs being deployed.

More uses coming for mobile robots

And there is plenty of scope for further growth. Up until now, warehousing has been highly dependent on human labor, and we are going to see 30,000 new warehouses being built over the next five years. But warehousing isn’t the only sector where we expect to see major penetration by mobile robots. Manufacturing, notably automotive, will also invest heavily in mobile robots in the next few years.

The automotive sector experience a catastrophic downturn during the pandemic, and recovery has been slow. As a result, investment in automated solutions declined. But the industry is at a turning point as manufacturers phase out internal combustible engine vehicle production, and reconfigure assembly lines for the era of the electric vehicle.

Automated solutions, including mobile robots, will play a significant part in this remodeling. One example is Arrival, are developing an entire AMR-based manufacturing concept, which they call the “microfactory,” for the efficient manufacturing of electric vehicles.

Automation imperative

The pandemic was a double-edged sword for the mobile robot sector. The spike in e-commerce, coupled with reduced throughput through enforced social distancing, increased the need for automation.

Yet at the same time, companies were reluctant to take the risk and invest. This resulted in a drop in mobile robot sales in the first half of 2020. But, that was only temporary.

It is evident that increasing levels of automation, including mobile robots, is key to addressing the continued scarcity of labor in warehouses. In addition, the continuing (and unprecedented) demands put on fulfillment centers and warehouses, in terms of volume, speed and efficiency requirements, will further drive mobile robotics deployments.

AMRs with higher payload capabilities are now being produced (up to 1,350 kg), and as a result, AMRs are becoming popular in manufacturing and other sectors for moving heavy loads.

The AMR advantage

While AMRs do not operate with the same precision or point-to-point speed as AGVs, AMRs do have certain advantages over AGVs. For example, there is no need for the operational infrastructure which AGVs require, and deployment can be much quicker.

AMRs, on the whole, are less expensive than AGVs. The average price for AMRs stands at approximately $20,000, compared with $75,000 for AGVs, and the purchase price of a small sortation AMR can be as little as $4,000.

AMRs have gained a particularly strong foothold for order fulfillment operations in logistics centers, where their autonomous navigation technology allows them to be deployed in a facility in large numbers. The ‘natural navigation’ technology employed by AMRs is being increasingly incorporated into other types of robotics and automation solutions, including AGVs.

AMRs with higher payload capabilities are now being produced (up to 1,350 kg or 2,976.2 lb.). As a result, AMRs are becoming popular in manufacturing and other sectors for moving heavy loads (pallet conveying, for example). In many cases, AGVs are being superseded by AMRs.

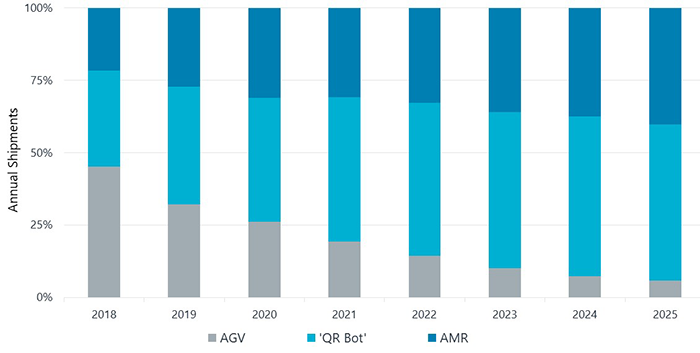

Figure 2: Forecast Share Shipments of AGVs vs AMRs. Source: Interact Analysis

Strong growth expected for mobile robots

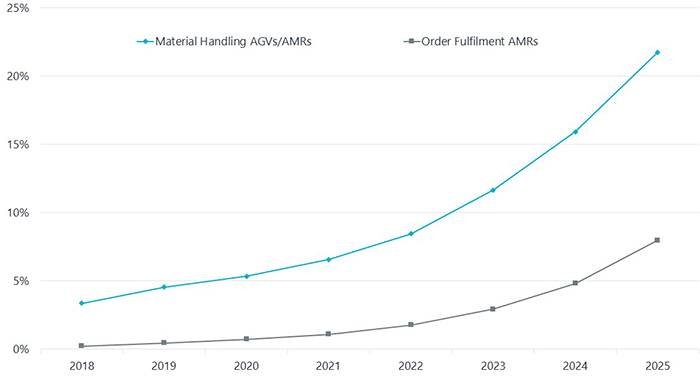

At the end of 2020, less than 1% of warehouses had deployed AMRs in support fulfillment operations (Figure 1). Material handling robots, which are a much more mature technology, were present in just over 5% of warehouses and manufacturing facilities. Going forward, AMRs are expected to demonstrate strong growth out to 2025 (Figure 2).

While AGVs still accounted for over 50% of all mobile robot revenues in 2020, this is expected to drop to under 25% by 2025. Meanwhile, AMRs that use QR codes for navigation, or QR bots, will actually account for 50% of all shipments throughout the forecast period, but their revenues are much smaller.

With 2.1 million mobile robots predicted to have been shipped by the end of 2025, including 860,000 in that year alone, generating annual revenues of $18 billion, the future looks exceptionally strong for AGV and AMR manufacturers.

Warehouse automation market still nascent

Despite several recent high profile acquisitions in the warehouse automation industry, talk of a period of upcoming consolidation is premature. The warehouse automation market is still at a nascent stage, and hence is open to technological innovation which continues to feed a growing number of new market entrants.

Editors Note: This article is reprinted with permission from Interact Analysis.

About the author

Ash Sharma, Managing Director, Interact Analysis

Ash Sharma (Ash.Sharma[AT]InteractAnalysis.com) has spent close to 20 years in technology research and is now research director for robotics and warehouse automation at Interact Analysis. In this role, he leads the company‘s market intelligence on the use of robots and other technology that enable intelligent automation, providing expert insight based on its research techniques. Sharma is also managing director at Interact Analysis, leading its Europe, the Middle East, and Africa (EMEA) operations.

In his previous role, Sharma served as vice president and senior Director at IHS Markit, where he led its power and industrial technology research practices. In this role, he led a team of more than 80 analysts providing market-leading research on several sectors, including industrial automation and smart manufacturing, smart home, solar power and energy storage, drones and robotics, medical technology and building automation. Sharma’s in-depth experience in these sectors and broad experience in market research and analysis helped establish Interact Analysis as a leader in intelligent automation research.