Source: SVB

Silicon Valley Bank, which has helped fund more than 30,000 startups, yesterday released a report on “The Future of Robotics: An Inside View on Innovation in Robotics.” It described trends in production, business models, and the adoption of robotics reflecting the increasing maturity of Industry 4.0. The report also addressed concerns about automation displacing jobs and public-policy reactions.

Overall, the free Silicon Valley Bank (SVB) report (download PDF) was cautiously optimistic about the prospects for industrial automation. It cited rising U.S. productivity, maturing technologies and suppliers supporting a variety of applications, and a steady climb for robotics deployments, particularly in Asia. The report also discussed the value of the robotics-as-a-service (RaaS) business model, in which automation becomes a recurring operating expense (OpEx) rather than a capital expenditure (CapEx).

SVB notes causes for concern

However, Santa Clara, Calif.-based SVB also observed that fewer but larger venture capital deals are being made. It described the potential for job displacement among less-educated workers, as well as policy proposals such as robot taxes and universal basic income (UBI).

“Recessions tend to reduce employment, and some jobs don’t come back,” said the report, which said that the COVID-19 crisis could accelerate economic shifts. “This trend is glaring for U.S. manufacturing in the prior two downturns, as businesses reconsidered their supply chains and looked to move production offshore or to automate. The pandemic’s effect on global supply chains has made the offshoring option problematic, increasing the likelihood that this cycle will see an increase in investment in automation.”

Discussing report details

Austin Badger, director of frontier tech at SVB and co-author of the report, replied to the following questions from The Robot Report:

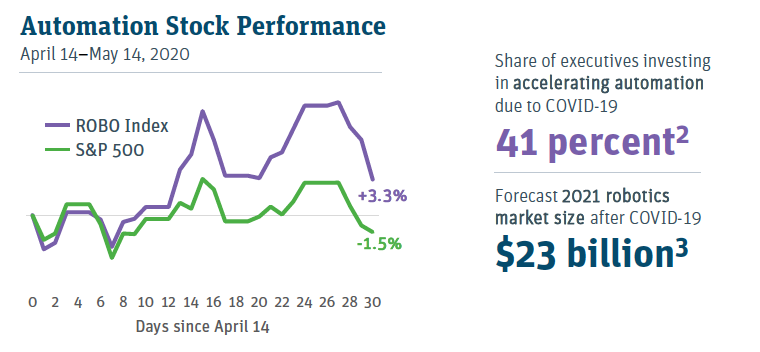

According to “The Future of Robotics,” automation stock performance has not increased overall by much, even though almost half of executives expect to invest in robotics. Is this then a longer-term trend?

Footnotes: 2. Based on Ernst & Young survey results, released 3/30/2020, 3. Based on ABI Research study relased 4/2/2020. Source: SVB

Badger: The focus of this insight is indeed the long term, but 4% relative performance versus the S&P [Standard & Poor’s index] during a bear market is certainly something to write home about. The dates shown cover a tumultuous time in the markets, as lockdowns persisted and the economy braced for recession.

It’s also highlighting the acceleration of a trend already in process. Actions that may have taken years are now occurring in months. Outsize performance is not to be expected in most categories, with the exception of some isolated segments such as remote work tech and some healthcare-related stocks.

With the Fourth Industrial Revolution upon us, what industries will automation affect most? Is it mainly manufacturing?

Badger: Industrial automation — manufacturing, construction, supply chain-related, and agriculture — are still the areas for which robotics is most relevant. These segments have seen the largest, most successful companies and the most notable exits.

However, we do expect Industry 4.0 to coincide with new growth in the consumer and service segments, with some key examples being food tech and frontier robotics companies.

The SVB report describes the increasing number of robots in China as “impressive” but “not tremendous.” What does that mean for robotics suppliers and users? Will other nations — such as the U.S. — pick up the slack?

Badger: The “not tremendous” comment alludes to the fact that 18% CAGR [compound annual growth rate] is a five-year doubling rate – likely too slow to support a massive industrial robotics industry if all firms are focusing on satisfying new demand.

Further, this growth is expected to halve over the next four years. Our take is that robotics suppliers will have an opportunity to build robots that replace the existing stock, as opposed to increasing the existing stock. This dramatically increases the TAM [total addressable market] in discussion. Consider that industrial robotics has been around for decades; thus, it is plausible that many robots on factory floors need an update.

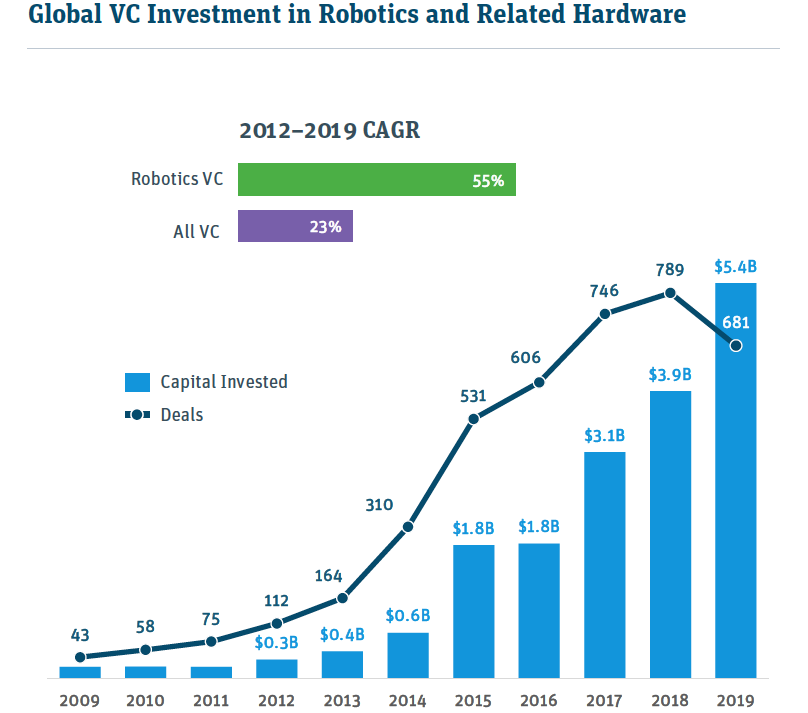

You mention emerging “category leaders” in robotics investments — can you give some examples? With fewer but bigger deals, what does this mean for innovation?

Sources: SVB, PitchBook

Badger: A climbing median deal size indicates that companies are maturing. As this occurs, we have seen specific segments become represented by a small handful of leading startups. For instance, Bossa Nova Robotics, 6 River Systems, Fabric, and a couple others are leading startups in industrial/supply chain.

As for innovation, this is an interesting problem. A strong early-stage environment encourages innovation by presenting competitive risk to established later-stage firms who want to avoid being usurped.

However, recent research at the NBER [National Bureau of Economic Research] showed that early-stage innovation is highly pro-cyclical – that is to say that recessions badly deplete innovation among early-stage companies – while later-stage innovation is more stable. Thus, more concentration at the late stage might make for more stable innovation in robotics in the coming years.

Also, it’s worth noting the late-stage stabilization occurs in all maturing markets, and has also been present in our recent data of overall VC investment.

The U.S. and China are leaders in venture capital investment. While China leads in robotics use, is the U.S. mainly exporting robots?

Badger: While data on orders for American-made robots is not public, we do know that China is by far the largest end user of industrial robots, with the U.S. market less than one-third as large.

One benefit of industrial automation, however, is its ability to enable production reshoring by achieving cost parity with cheaper labor abroad. This is another trend that could be accelerated by COVID-19 and could lead to rapid growth of the U.S. share of end users.

The SVB report discusses maximizing revenue per robot versus diversification — is this about commoditization, risk, or economies of scale?

Badger: Risk, specifically risk of a single contract cancellation causing a substantial drop in revenue.

You mention several major acquisitions, mostly around mobile robots in logistics and agriculture. Does this reflect maturity of the platforms or the readiness of each vertical for automation?

Badger: We interpret it as a reflection of large incumbents’ appraisal of later-stage robotics startups as competitive risks, as well as a confirmation of their innovative quality – essentially, their tech is worth the multi-hundred-million acquisition costs.

One chart in the report shows the decline in U.S. manufacturing productivity and employment — is it because of too much automation, or too little?

Badger: The chart shows that productivity and employment are inversely correlated – when productivity has gone up, employment has gone down. This is not a commentary on too much or too little automation. Generally, automation increases productivity. Many techno-optimists have assumed that this will naturally increase unemployment. In manufacturing, this has not been the case.

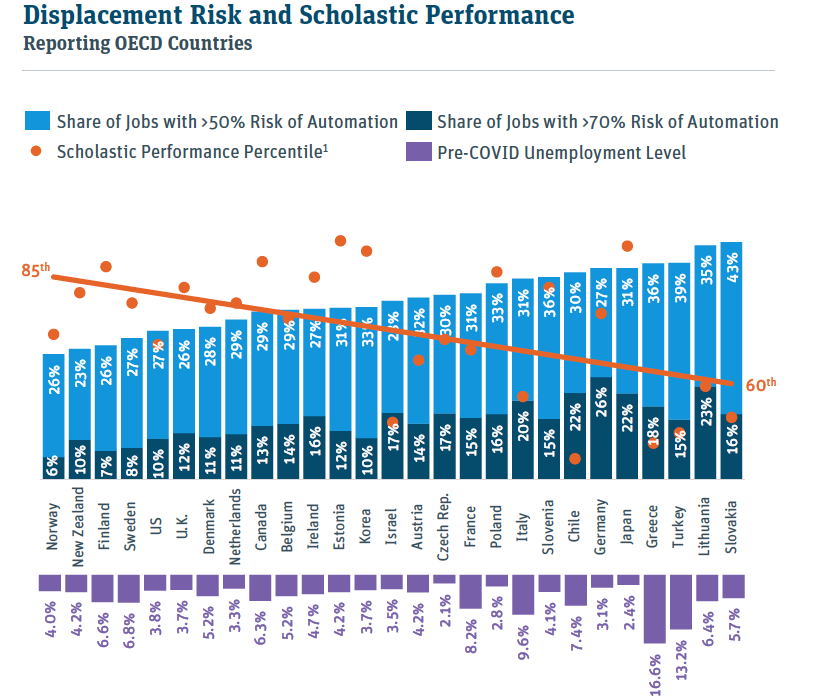

Where does the metric “Share of jobs with >50% or 70% risk of automation” come from? Aren’t low-skill jobs already vulnerable to offshore outsourcing?

Notes: 1) Measured by mean cumulative Programme for International Student Assessment (PISA) score. Percentiles based on all countries participating in the PISA assessment program, not just those shown.

Source: OECD, SVB

Badger: The automation risk data comes from the OECD [Organisation for Economic Co-operation and Development, which] characterized employment categories as more or less susceptible based on metrics like high or low skills, as you suggest. It is true that many low-skill jobs have already been offshored, but offshoring is not feasible for others, such as truck drivers.

The SVB report mentions the concept of how the introduction of automated teller machines (ATMs) did not initially lead to fewer bank jobs. Since both employment and automation have risen in the past few years, at least until the COVID-19 crisis, what’s the actual correlation between them?

Badger: In the case of the ATM, you have had continued growth in the automating technology — ATMs — but a decline in employment. We don’t have a general take on the relationship between automation and employment, but wanted to present a counterpoint to the ATM argument, which cites that the growth of ATMs did not reverse, but actually increased bank teller employment – this has ceased to be the case since the Great Financial Crisis.

Proponents such as Microsoft co-founder Bill Gates and presidential candidate Andrew Yang have proposed robot taxes and UBI in reaction to a growing wealth gap. How much of the current gap in the U.S. is attributable to automation or to other causes, such as tax policies?

Badger: The determinants of inequality are outside the scope of our research for this report, but there are strong arguments for both of the causes you mention.

Tell Us What You Think!